With warm weather and extended school breaks, summer is the perfect time for Americans to hit the road or take to the skies in search of rest and relaxation. Even amid rising fuel prices and ongoing economic uncertainty, more Americans are planning to travel this year. Numerator surveyed over 1,000 U.S. consumers about their summer vacation intentions and found that summer travel is rebounding in a big way, with both intent and spending on the rise.

Who is traveling this summer?

For summer 2026, 78% of Americans say they plan to take a summer vacation, a sharp increase from 61% who reported traveling in 2025. An additional 10% remain unsure, meaning nearly nine in ten consumers are at least considering a trip over the summer months. Among those planning vacations, commitment levels vary: about one-third (32%) have already booked their trips, while others are still actively planning or working out details.

- Millennials are the most likely to travel, with 83% planning a trip.

- Gen Z follows closely, with 78% saying that they will travel.

- Gen X and Boomers+ are tied, with 75% of each group saying they are going on vacation this summer.

Most travelers won’t be going alone. Nearly two-thirds (65%) of vacationers plan to travel with their spouse or partner, while 38% will travel with their children. Similar shares say they will travel with extended family (24%) or friends (21%).

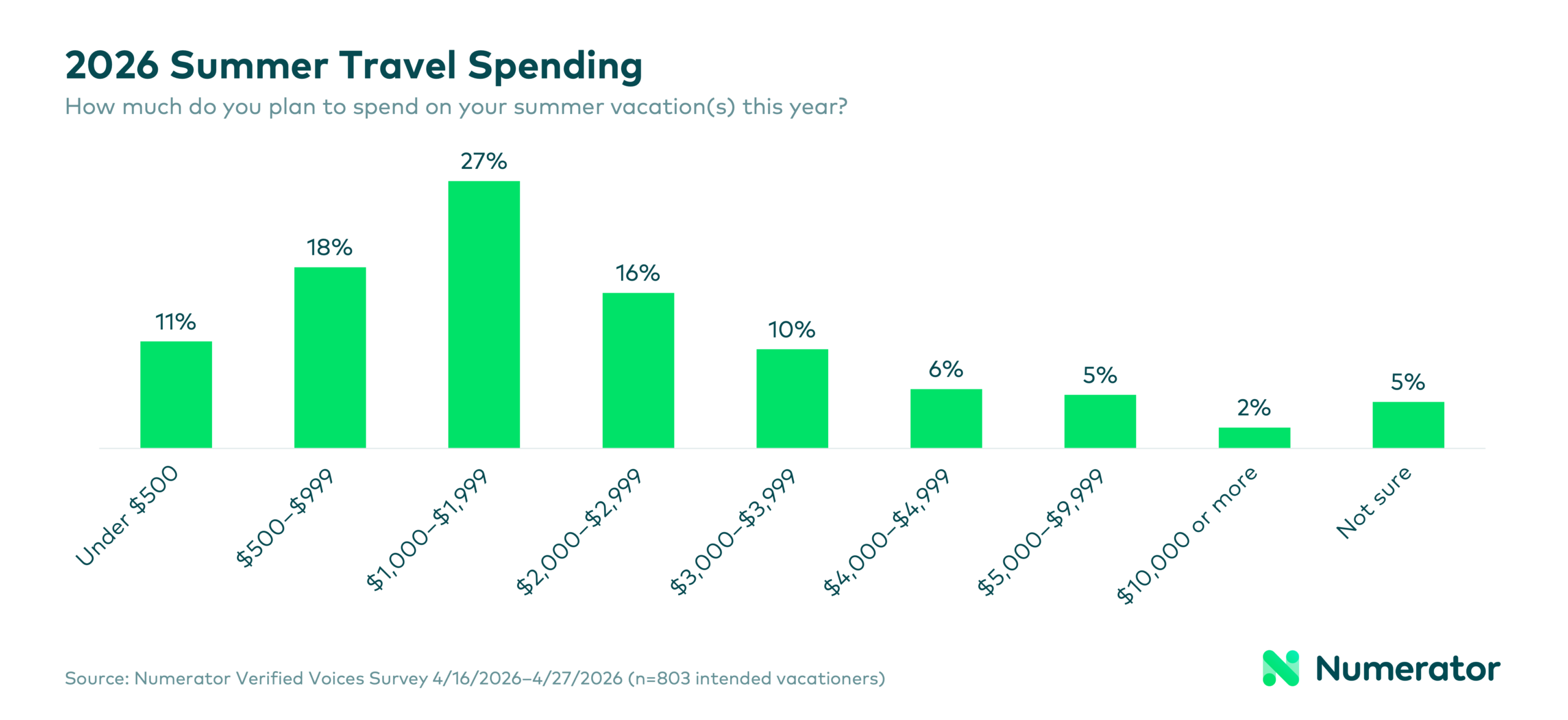

On average, U.S. vacationers plan to spend about $2,300 on their trips, putting total summer travel spending on track to reach as much as $525 billion—highlighting the magnitude of this seasonal rebound.

Where do Americans plan to travel this summer?

Most Americans will remain close to home this summer, with 80% of vacationers planning domestic trips. However, international travel is making a notable comeback. More than one in five travelers (22%) say they intend to travel abroad, representing a 10-point increase from 2025.

Interest in international travel is especially strong among Millennials and Asian consumers, who are more likely than average to plan trips outside the United States. At the same time, global travel brings additional concerns. Nearly two-thirds (63%) of international travelers report being at least somewhat concerned about anti-American sentiment abroad, with a small but meaningful share expressing high levels of concern (13%). These elevated worries are particularly pronounced among travelers from the Midwest (18%) and South (16%).

How are Americans getting to their vacation destinations?

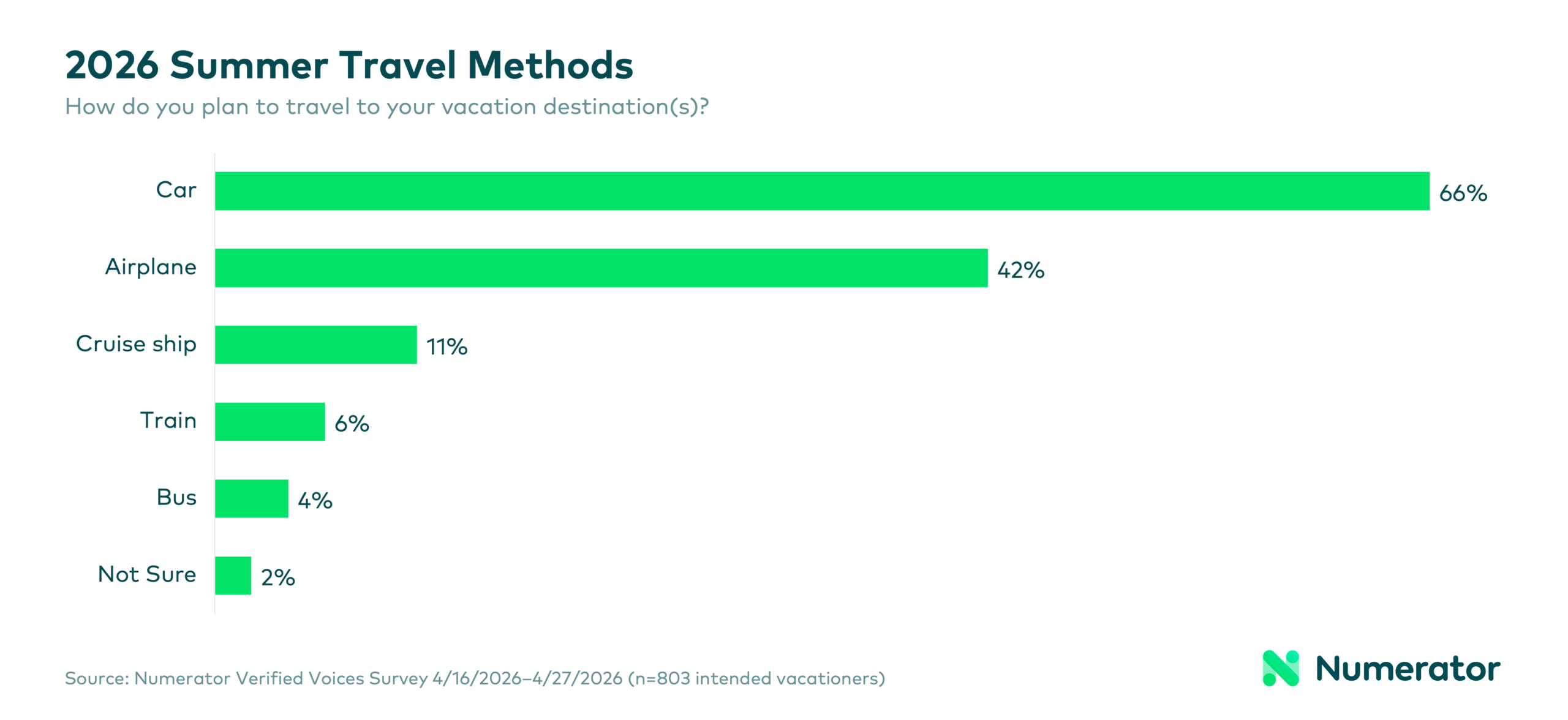

When it comes to getting to their destinations, most Americans still prefer to drive. About two-thirds (66%) of vacationers plan to travel by car, although this figure has declined slightly compared to last year. Air travel remains the second most popular option, with 42% of travelers planning to fly.

Geography plays a major role in transportation choices. Rural consumers are significantly more likely to rely on cars (77%), while urban residents are more inclined to fly (53%). However, recent events have deterred some vacationers from flying this summer. Two-fifths (40%) of those with non-flight travel plans originally intended to fly, but switched for various reasons, including high airfare prices (21%), concerns about long TSA wait times (16%), and worries about airline safety (13%).

Even among those who do plan to fly, concerns are widespread. 80% of flyers report at least one concern related to air travel, with many citing higher-than-expected ticket prices (51%) and TSA wait times (43%). Safety concerns and global events have also influenced some travelers’ plans, occasionally leading to route changes. Younger travelers, particularly Gen Z, are more likely to be affected by global conflicts and airport delays, while older travelers tend to focus more on airline safety.

What does a vacation look like for Americans in the summer of 2026?

Relaxation is the primary goal for 2026 summer vacationers, with the most popular types of trips being relaxation vacations (43%), beach vacations (33%), road trips (29%), nature / wilderness vacations (20%), and adventure vacations (19%).

These trips will take place across the entire summer, but mid-summer is the most popular timeframe. Among vacationers, July leads (43%), followed by late summer (August–September, 38%) and early summer (May–June, 37%).

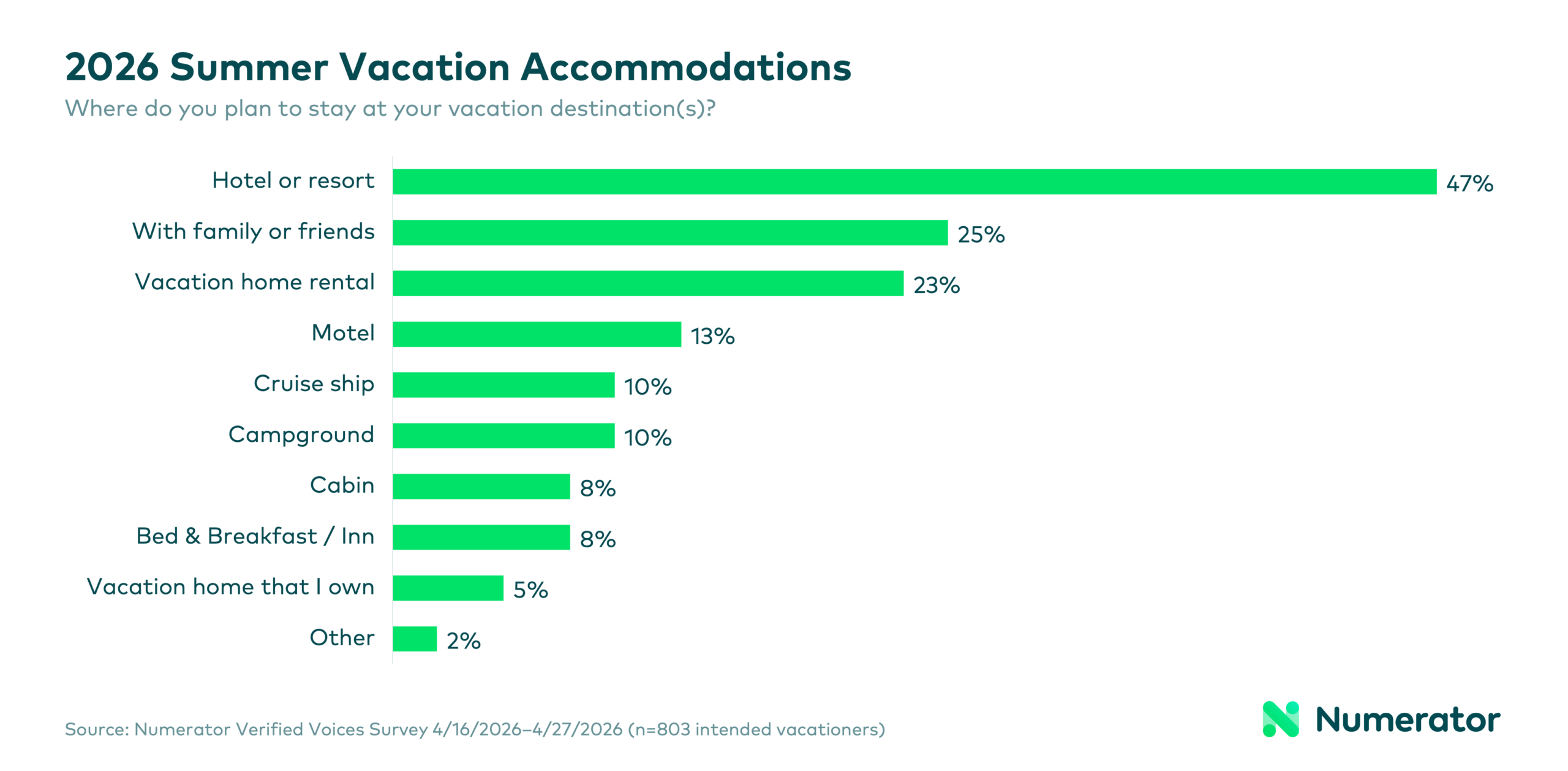

Deciding where to stay depends on budget, group size, and location needs. While hotels and resorts remain the most common option (47% of vacationers), many travelers are exploring alternatives. About one-quarter (25%) plan to stay with family or friends to save money, while a similar share is opting for vacation rentals for added space and flexibility (23%).

Demographics can also play a meaningful role in accommodation choice:

- Rural travelers are more likely to stay at campgrounds (13% vs. 10% overall), reflecting a preference for outdoor experiences.

- Asian travelers are more likely to stay with family or friends (35% vs. 25% overall), while Black travelers over-index on cruise ships (19% vs. 10%), suggesting a preference for all-in-one experiences.

- Low-income travelers are more likely to stay with family/friends (30% vs. 25%) and in motels (21% vs. 13% overall), highlighting more budget-conscious decisions.

- Households with children are more likely to stay in vacation rentals (26% vs. 23% overall), reflecting a need for space and flexibility.

What is stopping some Americans from traveling?

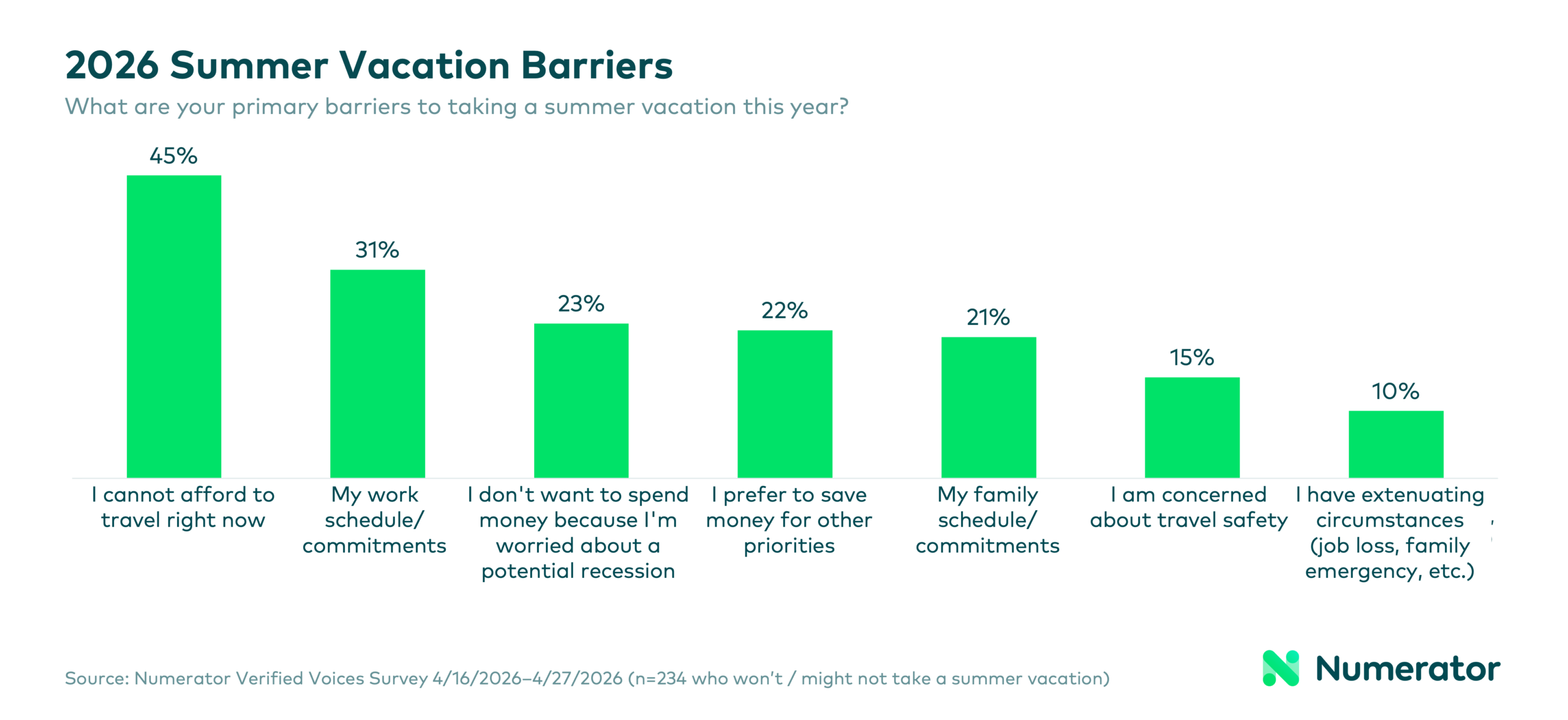

Despite strong demand, not everyone is able to take a vacation this summer. Financial constraints remain the top barrier, with 45% of non-travelers saying they cannot afford to travel. However, time constraints are becoming more significant. Nearly one-third (31%) of non-travelers cite work commitments, while about one in five (21%) point to family scheduling conflicts. Economic uncertainty also continues to play a role, with some consumers choosing to save rather than spend on travel (22%).

These challenges are not evenly distributed across demographics. Gen X consumers are particularly likely to cite affordability as a barrier, while Boomers are more focused on travel safety and potential disruptions. Households with children are significantly more likely to struggle with family scheduling logistics, and higher-income consumers—while less constrained by cost—are more likely to report work commitments as a limiting factor.

What are the key takeaways for the 2026 summer travel season?

Taken together, these findings paint a picture of a travel season defined by both optimism and practicality. Americans are eager to get away and are doing so in greater numbers than last year, but they are also making careful choices about how long they travel, how much they spend, and how they get there.

Rising intent, growing international interest, and evolving constraints all point to a dynamic summer travel landscape—one where consumers are balancing their desire for escape with the realities of cost, time, and an increasingly complex travel environment. For brands and retailers, this translates to more consumers on the move and more opportunities to meet needs across the journey. Travel-ready essentials, flexible pack sizes, and impulse-friendly offerings are likely to see increased demand as spending shifts toward experiences and on-the-go consumption.

Looking for more nuanced reasons behind travel decisions or interested in surveying your own verified buyers? Connect with your Numerator account partner or reach out to our team.